There's a lot to cover, so let's get right to our questions.

Who

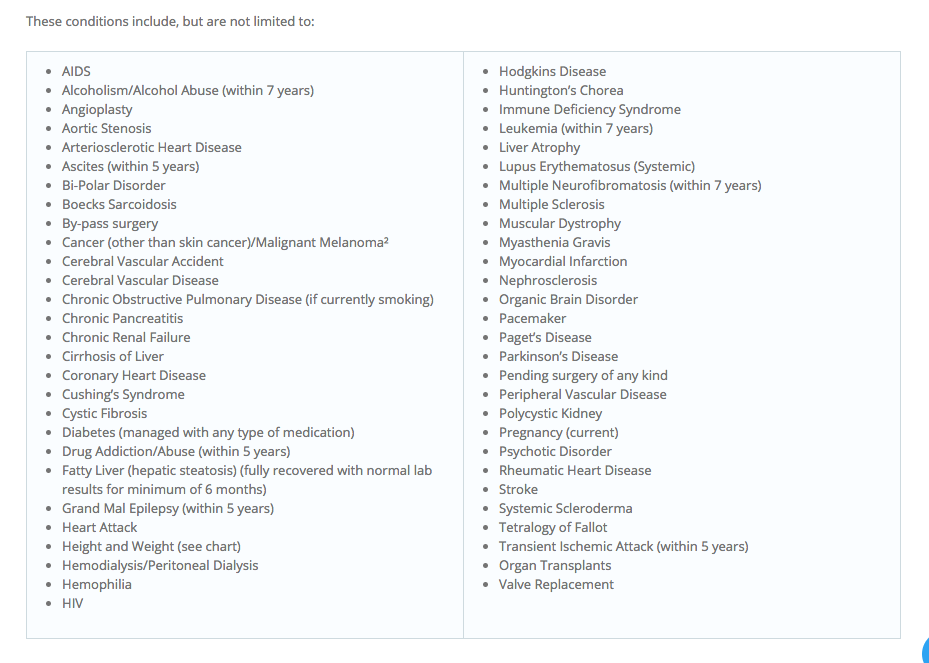

should check out these

lists

of possible pre-existing conditions that may prevent someone from receiving affordable insurance coverage for health care

if the AHCA is implemented*?

Everyone reading this, since nearly everyone who breathes will

eventually be slammed with one of these conditions—maybe not today or tomorrow,

but eventually, unless you inherited Jack Lalanne's genes.

Let's get right to it: Why should I have to cough up extra money for sick people when I could pay lower costs as a healthy person—or not buy insurance at all, if that's my choice?

We could do a deep dive into altruism and the greater good, or the

community-based philosophy that similarly drives why people without

kids pay school taxes or why non-military families pony up for veterans'

benefits, or why the underlying purpose of insurance is to buy it now when you don't need it so you have it when you suddenly and unexpectedly do need it, but those debates are for another time—not because I don't think those things are important and valid (oh yes I do), but just because most people in these crazy times have curled up in a fetal position and are now just wondering: How will all of this affect me? So let's look at this from a

purely selfish point of view, and I don't mean "selfish" in a bad

way—it's also practical and smart to look out for the needs of yourself and your

family. And it's our right as Americans to bitch about where our money goes. I

know I do!

The fact is, start saving up the money you think you're going to

be saving on premiums and deductibles with the AHCA, or by not buying insurance, and put it in a safe place,

because good luck avoiding all of the conditions on the potential pre-existing conditions

lists shown above, even if you're young and relatively fit (forget about the

rest of us). One of the only guarantees we have in life is that all of us are

going to get hurt or sick, in varying degrees, no matter how

"good" of a life we live.

But

the premiums are going to go down—that's one of the main points of this "repeal and replace" rigamarole.

The estimate on

the last AHCA proposal by the CBO and the Joint Committee on Taxation—there's

no current one yet, as this bill was rushed through before any thorough independent analysis could be completed—indicates

that premiums, on average, would first rise through 2020, then fall. But because

of the AHCA's new age-based ratings, those premiums would mainly fall for younger people,

as insurers would be able to charge older people five times more than younger

people.

Guess what, Class of '88 (those who make up much of my social

media circle): By insurable standards (and probably some other ones, too), we're

not considered spring chickens anymore—49 is the age when the premium rises I

mention will likely start to trend up, per an AARP

study. The AHCA is a pennywise/pound-foolish fix you'll likely regret down

the road. And that road is more like a short country path leading to the

mailbox for many of us, because that magic "49" is right around the

corner, if you haven't already hit it.

Insurers are also going to do whatever they can to hike premiums independent

of all of this, as insurers are wont to do—especially as they get

nervous about losing younger, healthier clients who would no longer have to

purchase insurance via the Obamacare mandate. Would those younger people eventually be drawn to purchasing insurance due to the ostensible cost savings to them through gouging older people? The AARP study extrapolates changing the age-rating system would have "only a modest impact on enrollment."

We'll have to see, I guess (though I hope we don't have to see, because I hope this plan dies a quick death with a DNR in place).

We'll have to see, I guess (though I hope we don't have to see, because I hope this plan dies a quick death with a DNR in place).

How

much will the premium surcharges run if the AHCA goes through and you have

certain pre-existing conditions?

You really don't want to know, but here

are some estimates (which would be based on various factors, obviously). If you're cool with possibly having to come up with $5,600 for diabetes

treatment, $17,000 for a pregnancy, $26,000 or so for arthritis and autoimmune

diseases, and between $28,000 and $140,000 for various types of cancers, then

this is the health care act you've been waiting for! (Actually, a bunch of patient advocacy groups say this isn't the health care act you've been waiting for.)

But

they've promised $8 billion extra to help those with pre-existing conditions

who will be placed in high-risk pools.

Yes. That $8 billion is included in the Upton

amendment, and it's not even close to providing adequate coverage for the

American people. While $8 billion seems like a lot of money, it would, in

combination with the $130 billion already slotted, help out only a fraction of

the people who would need it.

To put more specific numbers on it, in a simplified way (because this is much more complicated than I'm making it sound here): $138 billion would subsidize about 700,000 people

in high-risk pools a year. That would leave about 800,000 people in those high-risk

pools per year without reasonable access to affordable coverage. When this $8 billion number is thrown

out there to assure you everyone will be adequately covered, that is … not

true. Plus, more on how high-risk pools have failed in the past to provide

adequate coverage here

and here.

Well,

I have pretty good insurance through my employer, thank God.

Yeah, about that. Check out what the Wall

Street Journal calls a "little-noticed provision" that's

"part of a last-minute amendment" that, via state

waivers, would let insurers opt to dump coverage for 10

essential benefits mandated for coverage under Obamacare—good stuff like all your prescription meds, all your

pediatric visits if you have kids, PT and OT, trips to the ER, preventive

services if you have a chronic disease, inpatient care (in the hospital) and

outpatient care, and maternity and pregnancy care, among others:

Under the AHCA,

however, large employers would potentially have the option under those conditions to get rid of annual cost caps in their plans and also set in place

lifetime limits—meaning if you have a catastrophic illness or other major health snag, once your quota is

reached, you're SOL. It's not a given most employers would do so, but when times get tough and costs need to be cut, the option would be there. I've worked for enough employers to know that, pizza parties and free bagels in the cafeteria aside, my best interests are not always their top priority.

You

know, I'm looking back at these potential pre-existing conditions, because I need a break from all of your numbers, and they've got

some strange stuff listed. Pregnancy? Postpartum depression? C-sections? It's

almost as if women carrying and producing babies that were equally created by their

male partners would have to shoulder an unfair share of things on the financial

front.

Weird, right?

And

what about treatment for sexually transmitted diseases, mental health services, physical therapy, or whatever else a woman may need as a result of sexual assault or domestic violence incidents? Seems odd a woman could see her health care costs spike because someone else committed an act of violence against her**. You

could even speculate that women might be reluctant to report such incidents if they feel their health care coverage could be jeopardized.

You could speculate that, yes.

Not to change the subject, but I heard members of Congress are keeping Obamacare provisions for themselves while

trying to gut everyone else's. What's up with that?

Actually, an update: While there was an original

provision in the bill that provided for this, a separate piece of legislation

has since

been passed, meaning members of Congress will have to play by the same

health care rules as the rest of us, at least in the legal sense. How much better their wallets handle it over most of ours is another story.

So if this is such an eyebrow-raising thing for the American people, why were all those House reps laughing and celebrating with a

kegger*** in the Rose Garden after the AHCA vote?

Not sure, especially since the House vote is

just the first step in a long process. Maybe because they were excited about

the $765

billion tax cut over the next 10 years that will mainly benefit people in

their tax brackets and beyond. Or perhaps because they're just horribly tone-deaf people who either

have no clue or don't care that millions of people are despondent over this

proposal, with some not even sure they'd make it out alive if this goes through.

I'm assuming they don't know my friends who are

actually mulling the idea of moving out of the country because they don't know

what this would mean for their 13-year-old daughter with cystic fibrosis. They're

probably not familiar with my friend who has purchased life insurance for her

10-year-old son because he has Tetralogy of Fallot, or my former co-worker who

spends much of her spare time being an advocate for the Crohn's disease she

suffers from, or my cousin who has cerebral palsy. Who am I to say what

provoked such policy glee?

It can't be because they kept a campaign promise.

As I remember it, there were proclamations there would be no

cuts to Medicaid (there will be, to the tune of $370

billion over 10 years, at last estimate, shifting the burden to the states, which won't be able to pick up the entire load),

nonstop

talk of lower premiums and deductibles, plus "insurance

for everybody," including those with pre-existing conditions:

Not only

does the AHCA not keep these promises, it does pretty much the exact

opposite. The only fulfilled promise I'll concede (and only the first step

of it) is getting rid of something with "Obama" in its name.

I guess my point to the pols about their very

public merrymaking is: Have some decency. Spend a few minutes reading

some of the stories on the #IAmAPreexistingCondition

hashtag. Actually show up to your town halls and have conversations with your constituents to see how this will affect them. And take it to Paul Ryan's

basement in the dead of night the next time you want to whirl your noisemakers

over such a "victory." This isn't a victory for everyone—not by a

long shot, and you should be cognizant and respectful of that.

So

you're saying my concerns are completely invalid, you don't care if I have to

pay money I don't want to pay, and Obamacare is perfect?

I never said that; I don't want you to spend any more money than

you have to, hence this Q&A; and no, it isn't. Obamacare needs fixes. THIS IS NOT THAT FIX.

OK,

sorry, maybe I jumped the gun. But while this rant (whoops, sorry, did it

again!) of yours is entertaining, how about some immediately actionable items?

If you agree with what I've

said here: This stuff is getting thrown at us fast. Read up

on it, as boring as it seems—your future health, and that of your loved ones,

depends on it. If you'd like to make your views known to your elected

representatives on this week's AHCA vote, plug your zip code into the

Town Hall Project to find out when the next town hall near you is happening.

If you don't agree with what I've said

here: Same stuff I recommended above. In terms of actionable items, we may be looking for different results, so don't know that I can do any more of the heavy lifting for you here. And it's Friday—I need a

beer.

If

you're not sure what to think: I don't blame you. This

is all overwhelming, for all of us. I hope I didn't make it worse, but I'm hoping to make things better by offering resources that will give you the info you need to ensure a safe, healthy, affordable life for you and your family—no matter what side of the fence you're on.

If

you had to pick a favorite quote, what would it be?

I have a few, but let's go with: There but for the grace of God go

I.

FYI,

I skipped right to the end because I know you just went off on another one of

your liberal rants.

¯\_(ツ)_/¯ Good

luck with everything—and good health!

* What specific pre-existing conditions could be endangered if the AHCA bill goes through have not been set in stone. The BlueCross BlueShield site, however, has a banner over its previous list of pre-existing conditions that reads:

Other potentials mentioned in this post are ones culled from past pre-existing conditions lists from insurers or ones that experts feel could be reasonably anticipated to be dropped onto the list.

** The Washington Post gets more into the nuances of how rape and domestic violence themselves are not the pre-existing conditions that would preclude affordable insurance coverage, which is correct. However, the author, while acknowledging there's a path to significantly increased costs for women seeking treatment for the after-effects of these incidents (e.g., mental health services, STD treatments, physical therapy), glosses over that possibility to make it appear this shouldn't be a real concern, as certain conditions would have to be in place for this to happen.

The fact is, the path does exist to significantly increase costs (especially if women conceal that they were raped or abused, which is often the case), and it can be further widened with additional changes to the plan down the road. Also, try telling the women it would affect in these so-far limited conditions that this isn't a concern. We just went from "this never can happen" to "this sometimes can happen," and "sometimes" does not mean "rarely," especially in cases of underreported abuse and assault, where state laws would not offer the protections that the WaPo author mentions.

*** The rumor about the beer may have been just that: a rumor.

* What specific pre-existing conditions could be endangered if the AHCA bill goes through have not been set in stone. The BlueCross BlueShield site, however, has a banner over its previous list of pre-existing conditions that reads:

Other potentials mentioned in this post are ones culled from past pre-existing conditions lists from insurers or ones that experts feel could be reasonably anticipated to be dropped onto the list.

** The Washington Post gets more into the nuances of how rape and domestic violence themselves are not the pre-existing conditions that would preclude affordable insurance coverage, which is correct. However, the author, while acknowledging there's a path to significantly increased costs for women seeking treatment for the after-effects of these incidents (e.g., mental health services, STD treatments, physical therapy), glosses over that possibility to make it appear this shouldn't be a real concern, as certain conditions would have to be in place for this to happen.

The fact is, the path does exist to significantly increase costs (especially if women conceal that they were raped or abused, which is often the case), and it can be further widened with additional changes to the plan down the road. Also, try telling the women it would affect in these so-far limited conditions that this isn't a concern. We just went from "this never can happen" to "this sometimes can happen," and "sometimes" does not mean "rarely," especially in cases of underreported abuse and assault, where state laws would not offer the protections that the WaPo author mentions.

*** The rumor about the beer may have been just that: a rumor.

Tweets and treats at @jenngidman.